For homeowners with mortgages, rising insurance premiums pose a unique and unavoidable challenge. Unlike those who own their homes outright, mortgage holders are required by their lenders to maintain adequate homeowners insurance. This ensures that the lender’s investment in the property is protected in the event of a disaster, but it leaves homeowners with little choice but to absorb the increasing costs.

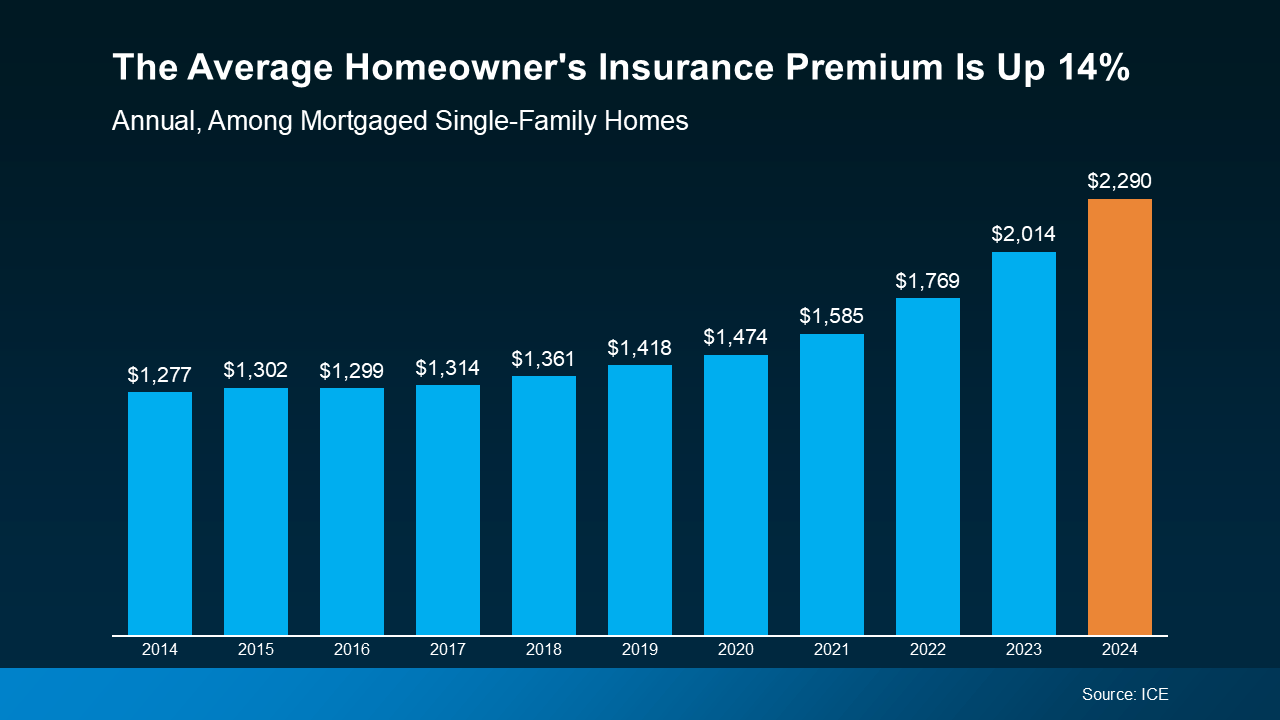

Between 2020 and 2023, insurance premiums surged by about 20%, and in some high-risk areas, the increases are even steeper. For many, this spike has strained household budgets, adding to the already heavy financial burden of rising interest rates, property taxes, and maintenance costs.

Several factors contribute to these rising costs:

- Climate Change: The increasing frequency and severity of natural disasters, such as hurricanes and wildfires, have resulted in higher claims, prompting insurers to raise premiums or withdraw from high-risk markets.

- Construction Costs: Between 2020 and 2023, construction input prices rose by 37.7%, with machinery costs increasing by 12% from 2022 to 2023, leading to more expensive claims for insurers.

- Regulatory Challenges: In some states, regulatory environments have hindered insurers’ ability to adjust rates in line with escalating risks, causing some companies to exit these markets.

Unfortunately, dropping coverage isn’t an option for mortgage holders. If a homeowner fails to maintain adequate insurance, the lender may purchase a policy on their behalf�often at a much higher cost�adding it to the homeowner’s monthly mortgage payment. This arrangement, known as “force-placed insurance,” typically provides less coverage at a premium rate, compounding the financial strain.

What Can Homeowners Do?

Homeowners feeling the squeeze have several strategies to mitigate the impact of rising insurance costs:

- Shop Around: Compare policies from multiple insurers to find the most competitive rates.

- Bundle Policies: Many companies offer discounts for bundling home and auto insurance.

- Increase Deductibles: Opting for a higher deductible can lower monthly premiums, though it means paying more out-of-pocket for claims.

- Explore State Programs: In some states, government-backed insurance programs may offer affordable options for high-risk homeowners.

A Call for Broader Solutions

While individual strategies can help, the broader affordability crisis requires systemic solutions. Climate change mitigation, regulatory reforms to stabilize insurance markets, and efforts to control construction costs are all critical to easing the financial burden on homeowners.

If you’re buying a home or already dealing with the strain of rising insurance costs, reach out to your insurance agent or lender to review your options, stay compliant with mortgage requirements, and safeguard your home and financial well-being.