It’s not really a surprise that 70% of buyers paused their home search last year. Maybe you were one of them. And if so, no judgment. Conditions just weren’t great.

Inventory was too low, prices were too high, and mortgage rates were bouncing all over. That made it really hard to find a home you loved – and could afford. And why sell if you’re not sure where you’re going to go?

But here’s the thing: the market’s shifting. And it might be time to hit play again.

The Inventory Sweet Spot

More homeowners are jumping back into their search to make a move this year. Builders are finishing more homes. And together, that’s creating more options for you when you move – maybe even the home you’ve been waiting for.

More homes = more possibilities.

But there’s more to it than that. When you sell, you don’t want to feel like it’s impossible to find your next home. At the same time, you also don’t want inventory to be so high, it takes ages for your house to sell. Right now, you’ll get the best of both worlds.

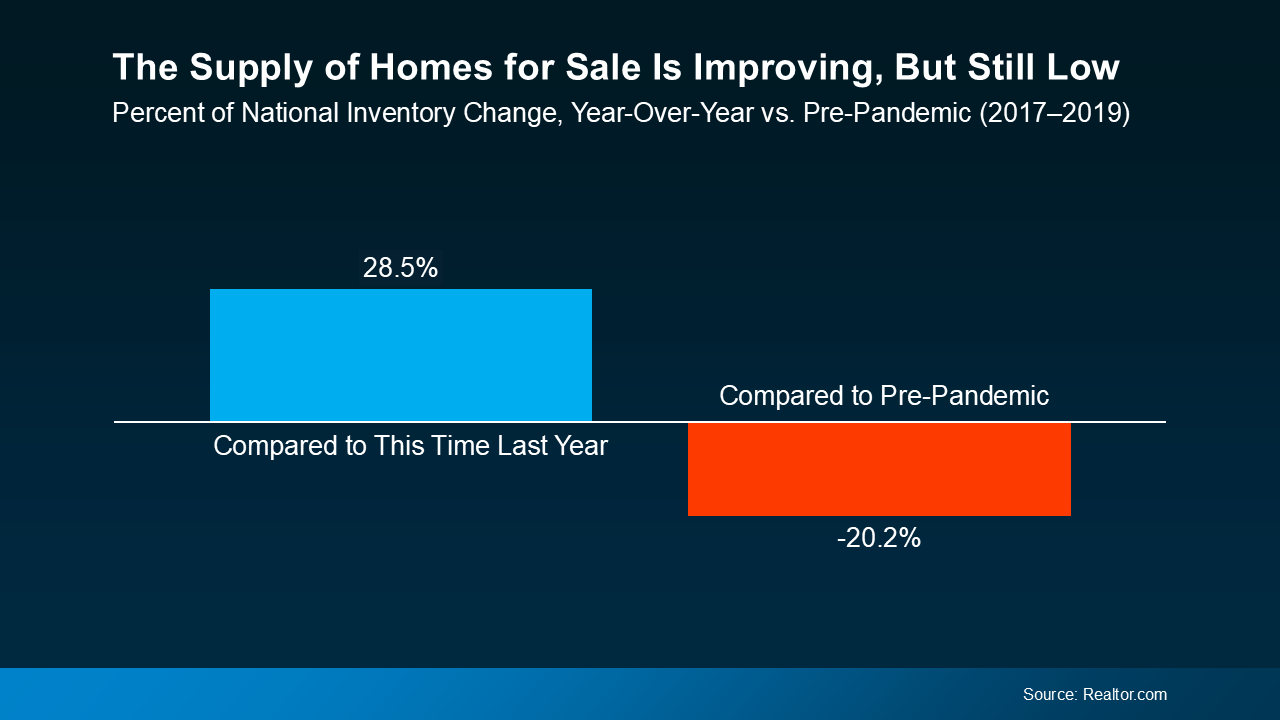

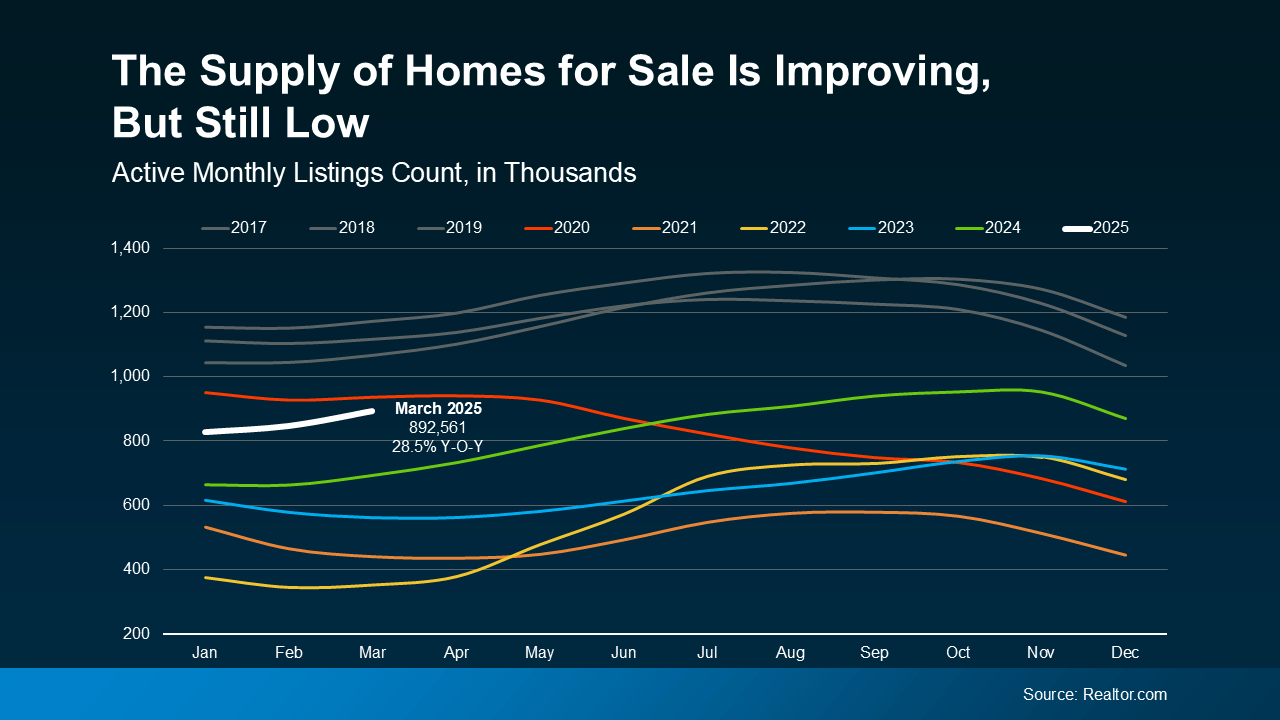

This data will help paint the picture for you. According to Realtor.com, inventory has jumped 28.5% since this time last year, but it’s still below pre-pandemic levels in most markets – and here’s why this is such a sweet spot (see graph below):

Basically, there are more homes to choose from when you make your move, but not so many that you’ll struggle to sell your current house. Your home should sell quickly if you work with an agent to make sure it’s priced right and prepped to impress.

Basically, there are more homes to choose from when you make your move, but not so many that you’ll struggle to sell your current house. Your home should sell quickly if you work with an agent to make sure it’s priced right and prepped to impress.

More options. Less chaos. Solid demand: That’s the real sweet spot.

But here’s something else to consider. Data from Realtor.com also shows inventory has been on the rise for 17 straight months. And experts agree it’s likely to continue climbing throughout the year. As Lance Lambert, Co-Founder of ResiClub explains:

“The fact that inventory is rising year-over-year . . . strongly suggests that national active housing inventory for sale is likely to end the year higher.”

So, this may actually be the best time to sell. Your house may stand out more now than it would as the year goes on and inventory grows even more. Wait too long, and you may be one of many trying to stand out later this year.

Bottom Line

If you’ve been waiting for the housing market to give you a sign – it just did. Whether you’re looking to move up, scale down, or relocate completely, this might be the best balance we’ve seen in a while.

What’s holding you back from taking advantage of this sweet spot? Let’s talk through it and see what’s possible.

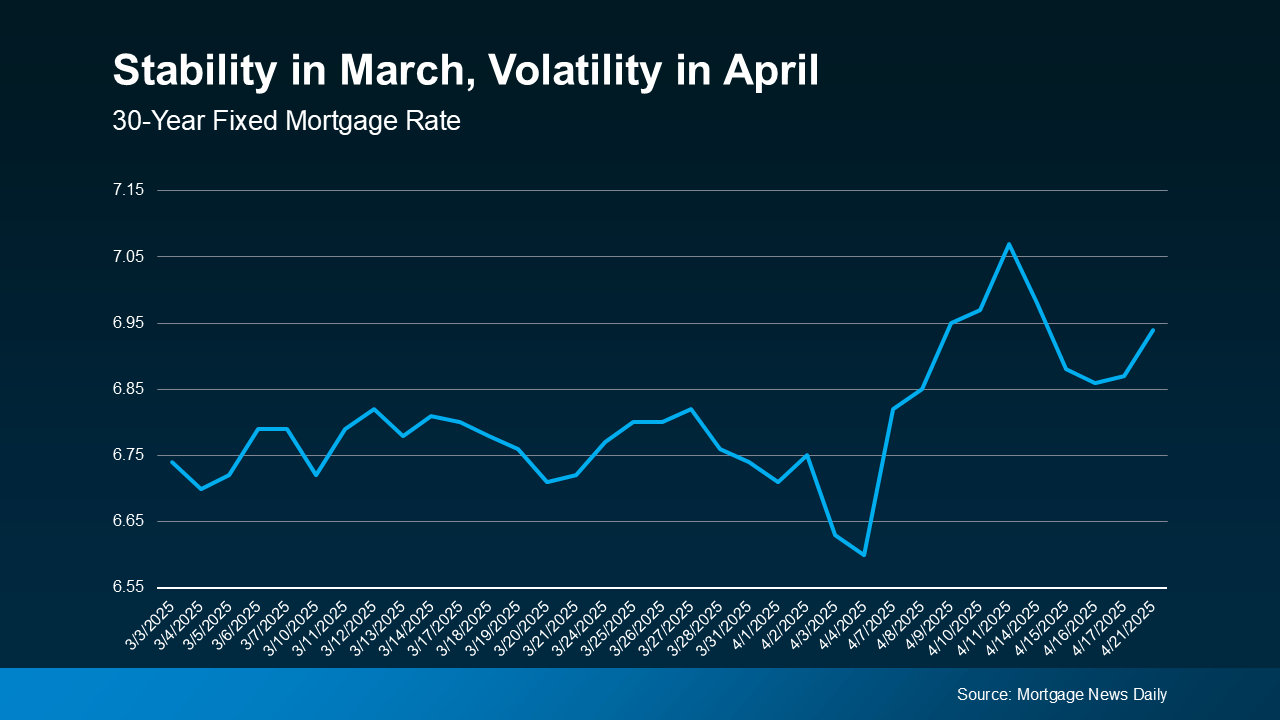

This kind of up-and-down volatility is expected when economic changes are happening.

This kind of up-and-down volatility is expected when economic changes are happening.

For anyone who’s been waiting for more choices, this is exactly what you’ve been hoping for – because more homes coming onto the market means more options and a better shot at finding one that fits your needs.

For anyone who’s been waiting for more choices, this is exactly what you’ve been hoping for – because more homes coming onto the market means more options and a better shot at finding one that fits your needs.