Selling your current home before buying a new one can feel like a delicate balancing act. The challenges of juggling showings, deadlines, and temporary housing often add unnecessary stress to an already overwhelming process. But what if you could buy your new home before selling your current one? Thanks to recent changes in underwriting guidelines, this is now a reality for many sellers.

The “Buy Before You Sell” program offers a solution to common pain points:

- No Contingency Offers: Offers contingent on selling your current home are often less attractive to sellers. With this program, you can make competitive, contingency-free offers.

- Less Disruption at Home: Avoid inconvenient showings and the need to keep your home meticulously staged while balancing daily family life.

- Time to Secure a Better Offer: Without the pressure of deadlines, you can hold out for a strong offer on your current home rather than settling for less.

- Freedom to Find Your Dream Home: You don’t have to rush to buy a home that isn’t the right fit just because time is running out.

- Avoid Lease-Back Clauses – Skip the complications of negotiating lease-back agreements with buyers.

- No Temporary Housing or Double Moves – Eliminate the hassle of renting or finding short-term housing and avoid moving twice.

- Easier Home Staging – Once you’ve moved out, you can neutralize your home’s d�cor, making it more appealing to a broader range of buyers.

- Quicker Sales and Higher Prices – Vacant homes not only sell faster but often for higher prices when presented neutrally.

The “Buy Before You Sell” program provides significant advantages to sellers:

- Access to Home Equity – Sellers can unlock some of their current home’s equity to fund the purchase of their new home.

- Debt Flexibility – Lenders may exclude your current mortgage payment from debt calculations when underwriting the new loan, which can make qualifying for your next home easier.

- More Time and Control – The program gives you the freedom to manage your timeline, reducing stress and allowing for well-thought-out decisions.

A Stress-Free Transition

This approach not only relieves the financial and logistical pressures of selling but also gives you the flexibility to make the best decisions for your family. It ensures that you’re not compromising on your next home or your selling price and allows for a smoother, more comfortable transition into your new space.

If you’re planning to sell your current home and buy a new one, ask your real estate agent or trusted lender about the “Buy Before You Sell” program. It could be the key to a stress-free, seamless move.

If you need a recommendation for a trusted mortgage lender who can help you buy before you sell, give me a call. And of course, we will be happy to provide you with a complimentary market analysis so you’ll know how much equity you have available.

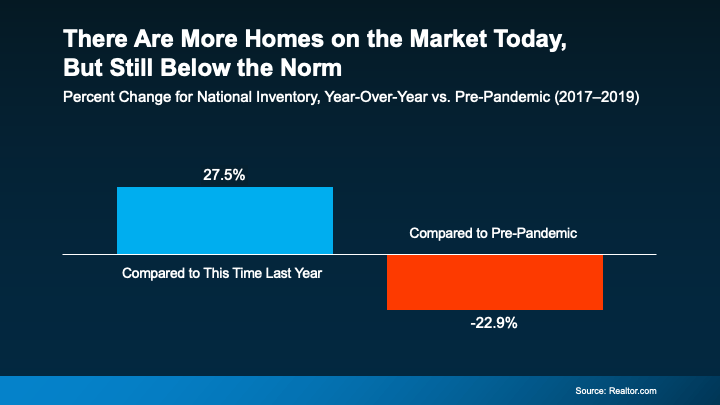

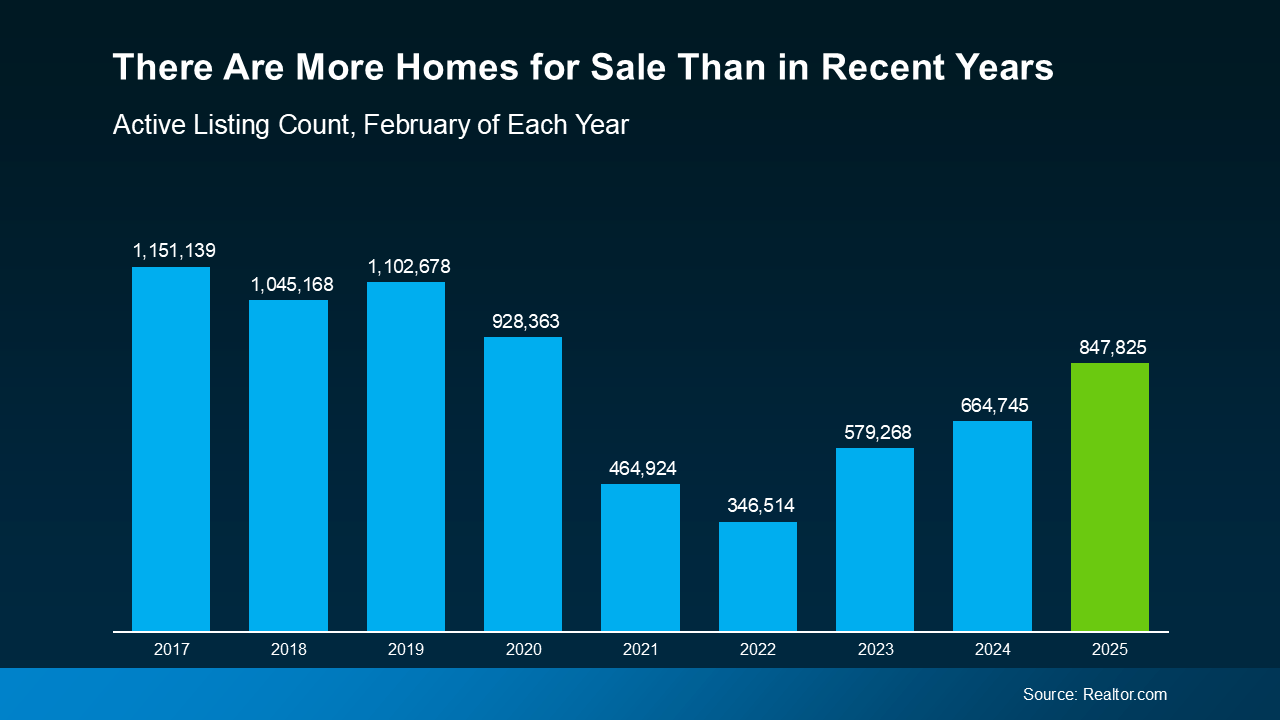

For anyone who’s been waiting for more choices, this is exactly what you’ve been hoping for – because more homes coming onto the market means more options and a better shot at finding one that fits your needs.

For anyone who’s been waiting for more choices, this is exactly what you’ve been hoping for – because more homes coming onto the market means more options and a better shot at finding one that fits your needs.

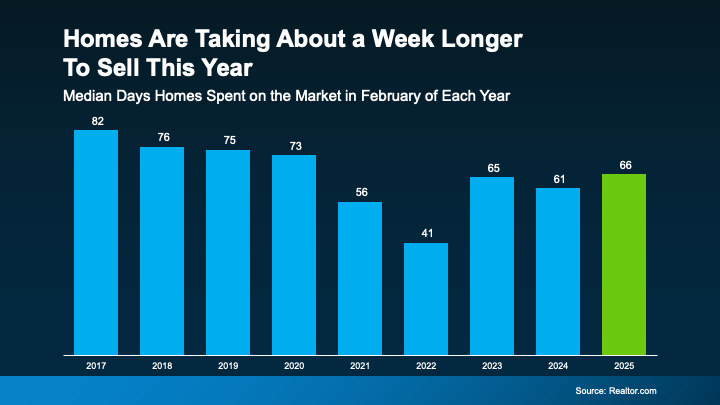

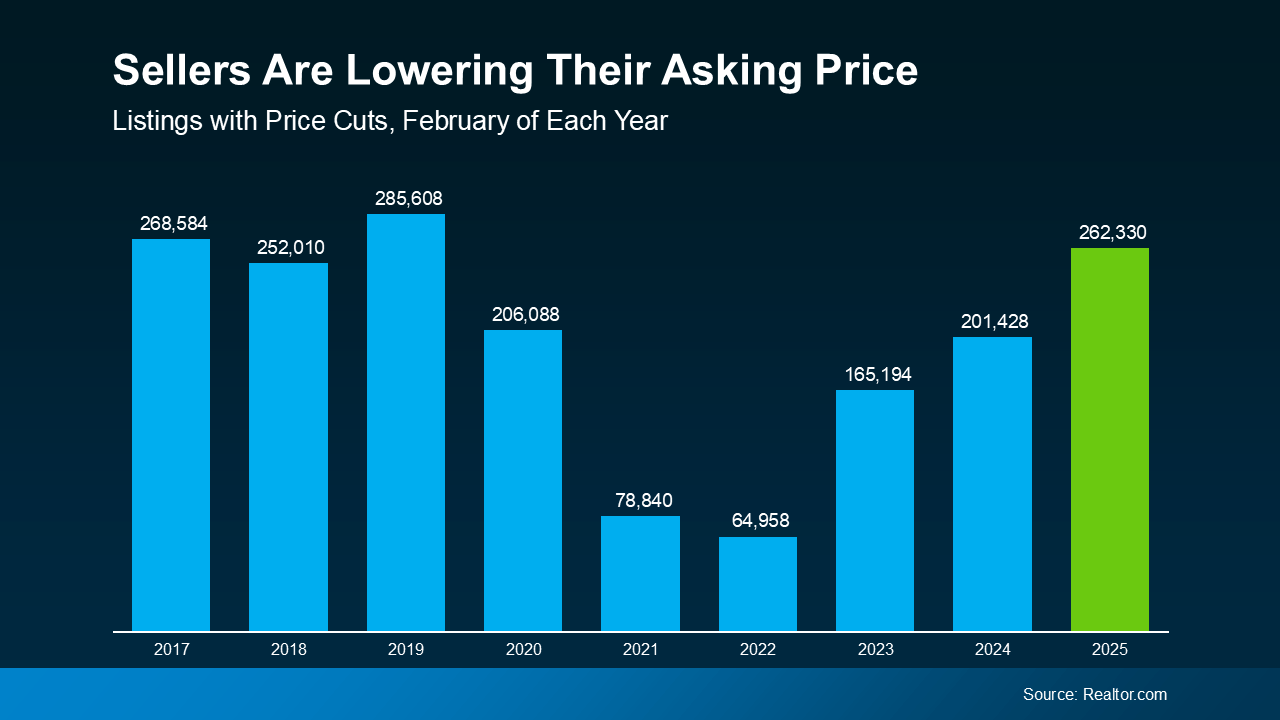

This is a sign sellers are more willing to compromise today. If you look back to more normal years in the market (2017–2019), you’ll see that the number of price cuts happening today is much closer to what’s typical – and for most buyers, that’s a big relief.

This is a sign sellers are more willing to compromise today. If you look back to more normal years in the market (2017–2019), you’ll see that the number of price cuts happening today is much closer to what’s typical – and for most buyers, that’s a big relief.