In today’s fast-paced real estate market, homeowners are increasingly considering alternative selling methods. One option gaining traction is selling to an iBuyer company. These tech-driven real estate firms offer a quick, streamlined process for homeowners looking to sell their properties. But like any major financial decision, selling to an iBuyer comes with its own set of advantages and disadvantages. Let’s explore the key factors to consider when weighing this modern selling approach against traditional methods.

Pros of Selling to an iBuyer

Speed and Convenience – iBuyers have revolutionized the selling process by offering remarkably fast transactions, often closing within 10-14 days. This rapid turnaround is a game-changer for sellers who need to relocate quickly or want to avoid the prolonged process of traditional home selling. It’s particularly appealing for those facing time-sensitive situations like job transfers or family emergencies.

Simplified Process – The iBuyer model has transformed the home selling experience into a predominantly online transaction. This digital approach eliminates the need for time-consuming tasks such as staging, hosting open houses, and accommodating multiple showings. For sellers who value privacy or have hectic schedules, this streamlined process can be a significant relief, allowing them to sell their home with minimal disruption to their daily lives.

Cash Offers – One of the most attractive features of iBuyers is their ability to make all-cash offers. This financial flexibility can be a crucial advantage for sellers who need immediate liquidity or are looking to make a contingency-free offer on their next home. Cash offers also typically mean faster closings and fewer potential complications, providing sellers with a higher degree of certainty in their transactions.

As-Is Purchase – iBuyers often purchase homes in their current condition, without requiring sellers to make repairs or upgrades. This feature can be particularly beneficial for homeowners with properties in less-than-perfect condition or those who lack the time or resources to prepare their home for traditional market listing. It allows sellers to avoid the stress and expense of pre-sale renovations, which can be substantial in some cases.

Cons of Selling to an iBuyer

Lower Sale Price – While iBuyers offer convenience, it often comes at a cost. These companies typically offer below-market prices for homes, with sellers potentially receiving less than they might through traditional methods. This pricing strategy allows iBuyers to quickly resell properties for a profit, but it means sellers may be leaving money on the table. In hot markets or for unique properties, this difference could be even more significant.

Higher Fees – The convenience of iBuyer services often comes with higher transaction fees compared to traditional real estate commissions. These fees can reach up to 13% of the home’s price, significantly eating into the seller’s proceeds. While traditional real estate commissions typically range much less, iBuyer fees encompass various services and risk factors, resulting in a higher overall cost to the seller.

Limited Negotiation – iBuyers rely heavily on computerized models to determine offer prices, leaving little room for negotiation. This approach means sellers are often presented with a take-it-or-leave-it offer, unlike in traditional sales where there’s often back-and-forth between buyers and sellers. For homeowners who believe their property has unique value or features that an algorithm might not capture, this lack of flexibility can be frustrating.

Lack of Representation – When selling to an iBuyer, homeowners forgo the personalized guidance and local market expertise that comes with working with a real estate agent. While this might appeal to some, others may miss the nuanced advice and emotional support that an experienced agent can provide throughout the selling process. This lack of personal interaction and the fiduciary relationship with an agent can be particularly challenging for first-time sellers or those dealing with complex property situations.

Availability Limitations – iBuyer services are not universally available and often have specific criteria for the homes they purchase. This limitation means that many homeowners, particularly those in rural areas or with unique properties, may not have access to this selling option. Additionally, iBuyers typically focus on homes within certain price ranges and conditions, further restricting their availability to a subset of the market.

While selling to an iBuyer offers undeniable convenience in terms of time and effort, it’s crucial for homeowners to recognize the financial trade-offs involved. The streamlined process and quick closing can be attractive, especially for those in time-sensitive situations.

However, the convenience often comes at the cost of a discounted sale price, potentially resulting in sellers not realizing the maximum equity from their homes. Homeowners must carefully weigh the value of a faster, easier sale against the possibility of a higher return through traditional methods.

Ultimately, the decision should align with the seller’s specific circumstances, financial goals, and market conditions. For those prioritizing top dollar over speed, working with a skilled real estate agent to navigate the traditional market might be the better choice to maximize their home’s value.

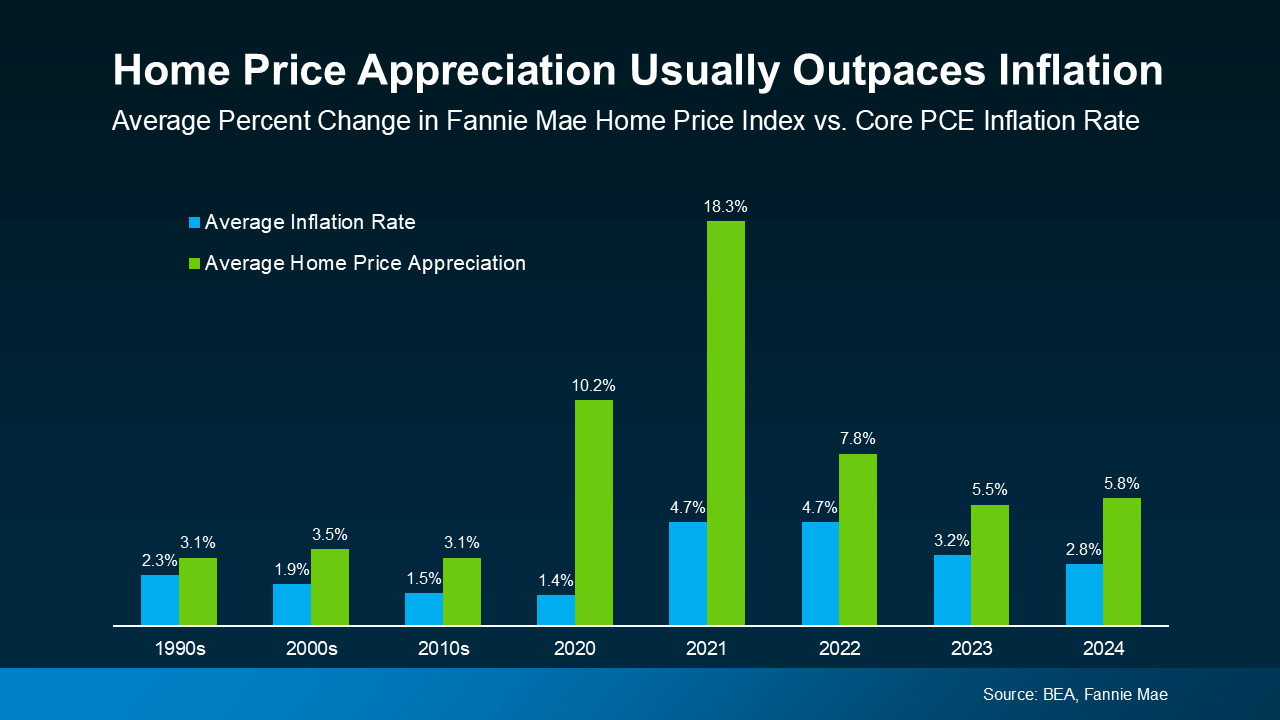

If you’ve been holding off on selling because you were worried about buying your next home at today’s rates and prices, let that sink in. It may be more than enough to help close the affordability gap and get you into your next house.

If you’ve been holding off on selling because you were worried about buying your next home at today’s rates and prices, let that sink in. It may be more than enough to help close the affordability gap and get you into your next house.

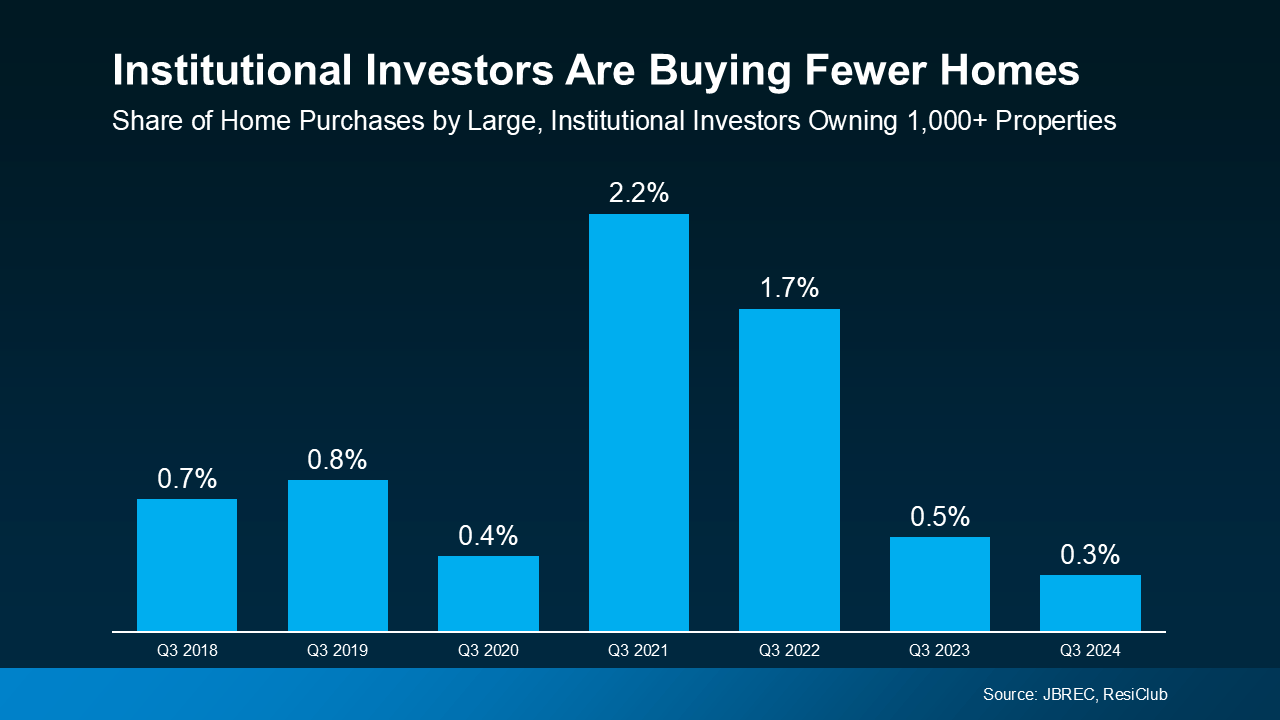

That’s a major shift, and it means far fewer investors are competing in the market now than just a few years ago.

That’s a major shift, and it means far fewer investors are competing in the market now than just a few years ago.

And

And