Waiting for perfect market conditions often means missing out. Because what you may not realize is, if you’re ready and able to buy, this time of year could actually give you an edge. Here’s why. As the weather cools down, the housing market can too – and that works in your favor.

You Likely Won’t Feel as Rushed

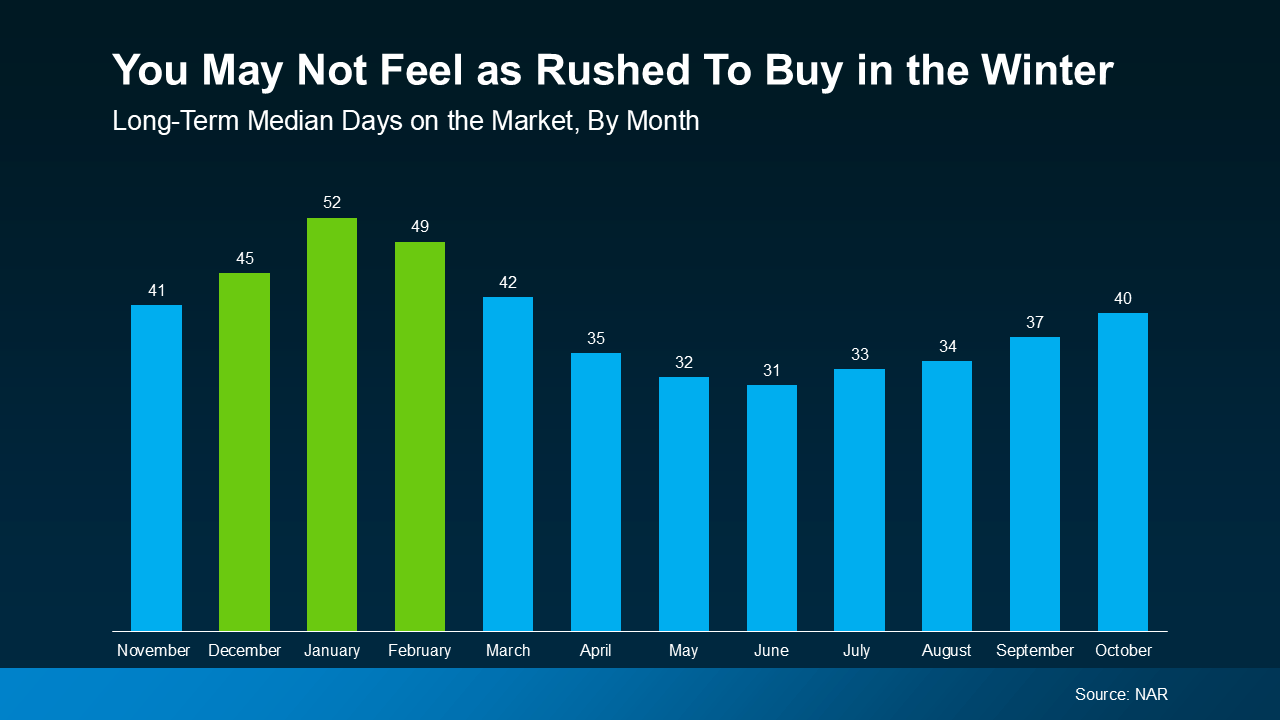

Homes tend to take a little longer to sell during this time of year. Data from the National Association of Realtors (NAR) shows the average time a house sits on the market jumps up during the winter months (see the green bars in the graph below):

This is partly because fewer buyers are active at this time of year – and that decrease in buyer competition means the houses that are on the market aren’t going to be snatched up as quickly. So, if you decide to buy a home in the next couple of months, you’ll likely have more time to consider your options and negotiate a deal without feeling as pressured.

This is partly because fewer buyers are active at this time of year – and that decrease in buyer competition means the houses that are on the market aren’t going to be snatched up as quickly. So, if you decide to buy a home in the next couple of months, you’ll likely have more time to consider your options and negotiate a deal without feeling as pressured.

Sellers May Be More Willing To Negotiate

And since homes generally take longer to sell during the winter, sellers are often more motivated to close a deal. That can work in your favor, too. According to NAR:

“Less competition can lead to better deals. While homes are not selling as fast as during the summer, sellers may be more willing to negotiate.”

Whether it’s compromising on price, covering closing costs or repairs, or including extras like appliances, you have more room to ask for what you need.

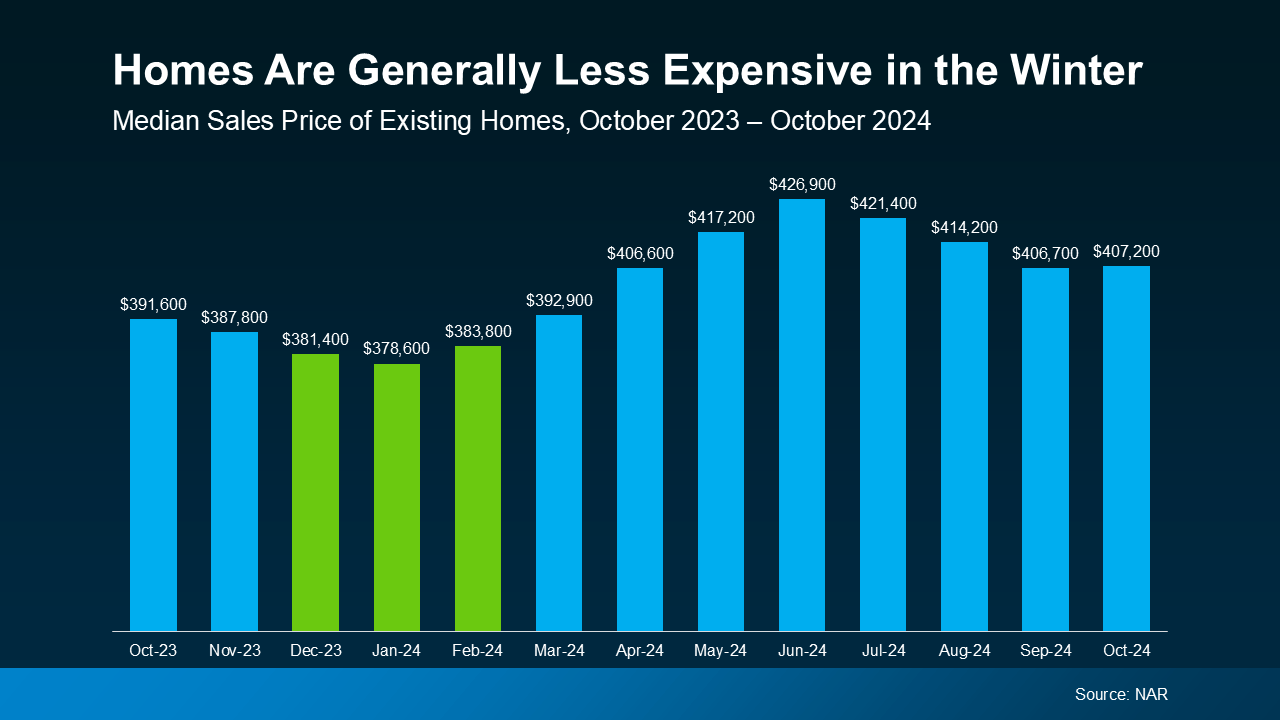

Homes Are Less Expensive in the Winter

With less competition from other buyers and sellers who are more willing to negotiate, you may see slightly lower prices too. In fact, according to NAR, homes are typically about 5% less expensive now compared to when prices normally peak in the summer.

That might not seem like a huge difference, but on a $400,000 home, it could mean savings of $20,000 on the purchase price.

You can see this expected seasonal shift in home prices taking place this year. Take a look at the graph below showing the median sales price of existing homes (homes that were previously owned) over the past 12 months. You’ll notice in the green bars that prices were lower in the winter months last year, and it seems like that’s going to happen again this year. That gives you the chance to make your budget go further:

Bottom Line

Buying a home during the winter means less competition, motivated sellers, and potentially lower prices, too. Let’s work together to find the right one at the right price for you.