Lately, it feels like every headline about the housing market comes with a side of doubt. Are prices going up or down? Are we headed for a crash? Will rates ever come down? And all the media noise may leave you wondering: does it really make sense to buy a home right now?

But here’s one thing that doesn’t get enough airtime. Real estate has always been about the long game. And when you look at the big picture, not just the latest clickbait headlines, it’s easy to see why so many people say it’s still the best investment you can make – even now.

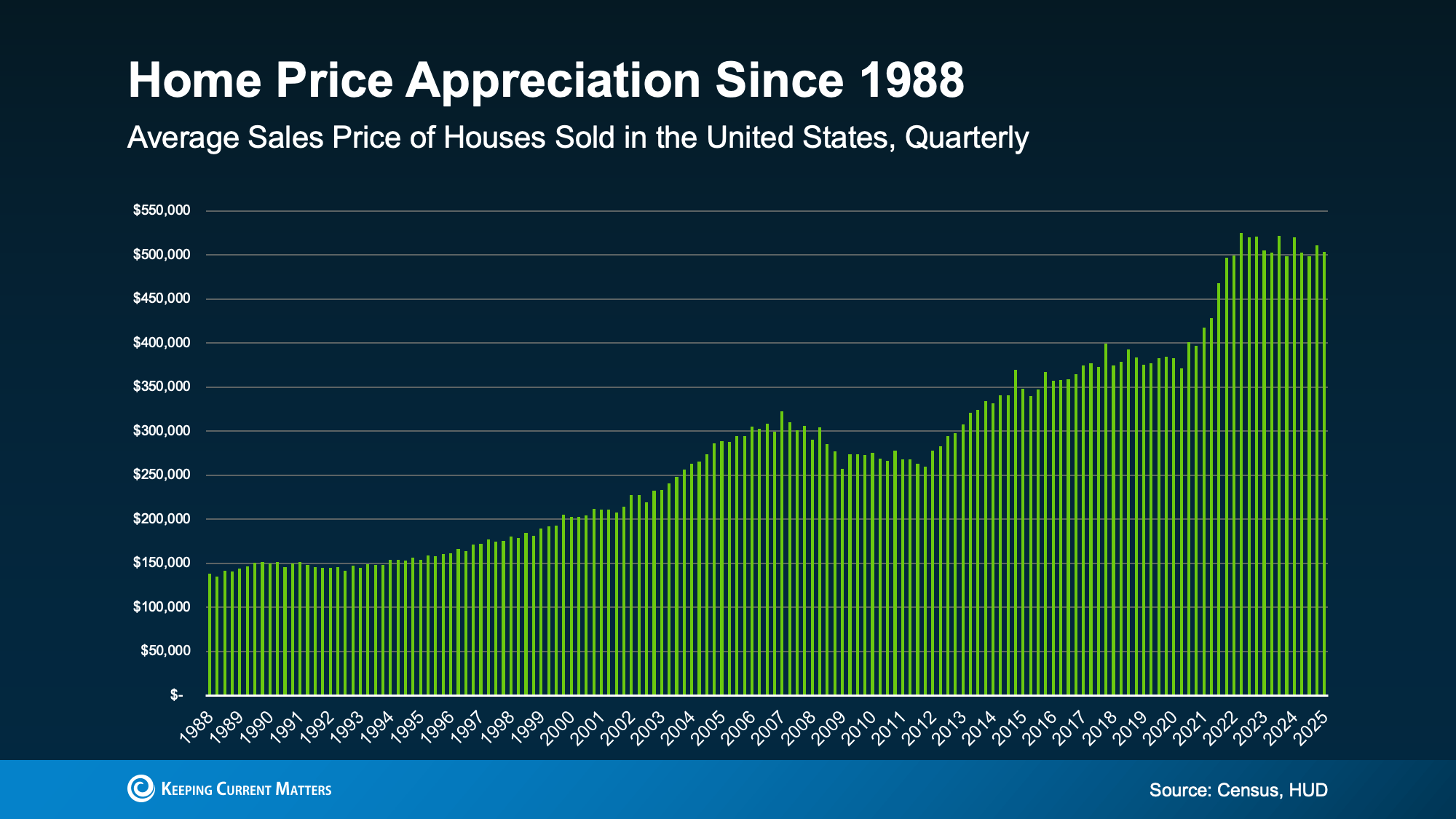

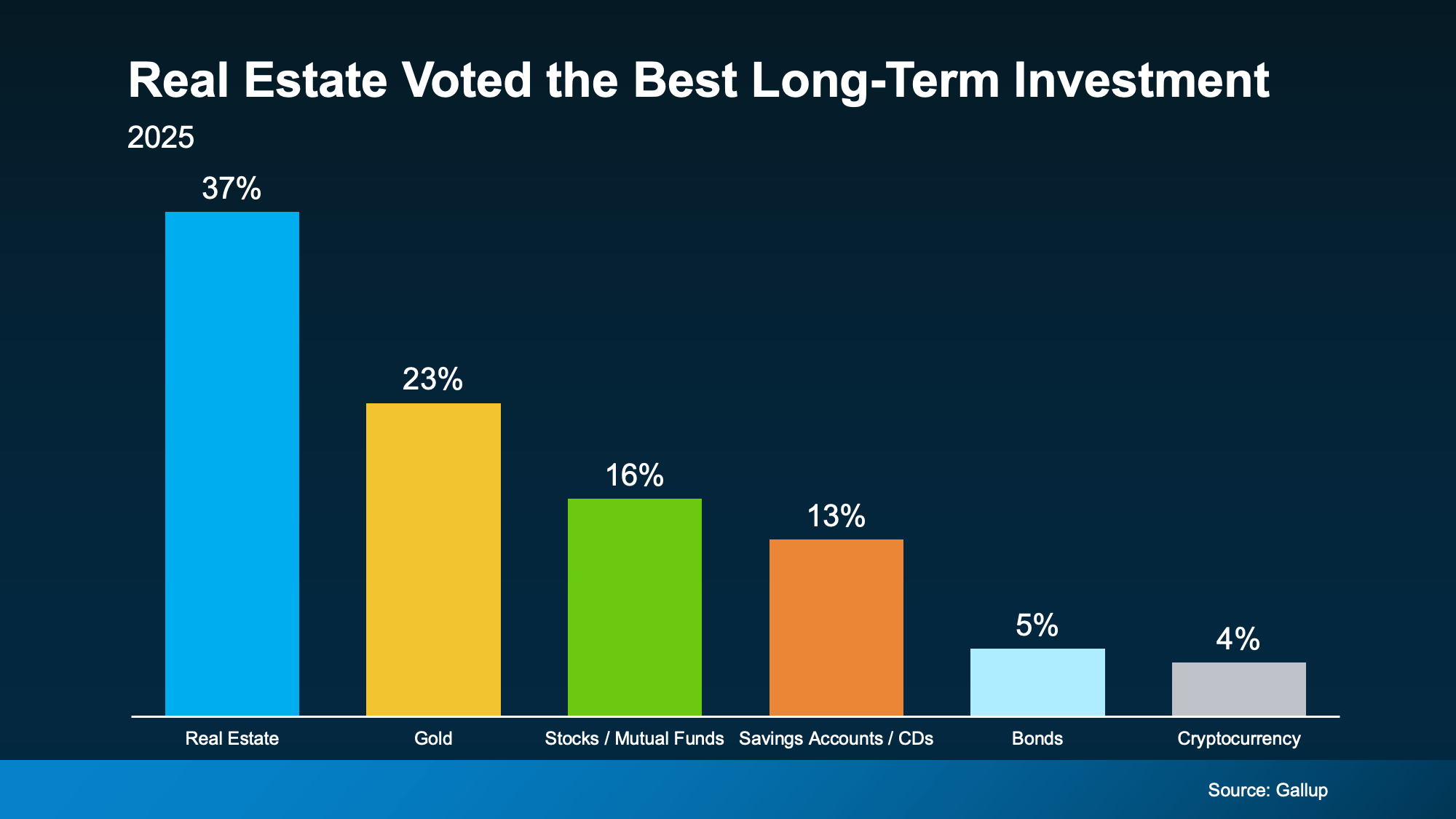

According to the just-released annual report from Gallup, real estate has been voted the best long-term investment for the 12th year in a row. That’s over a decade of beating out stocks, gold, and bonds as America’s top pick.

And this isn’t new. Real estate usually claims the #1 title. But here’s what’s really interesting. This year’s results came in just after a rocky April for the stock and bond markets. It shows that, even as other investments had wild swings, real estate has held its ground. That’s likely because it gains value in a steadier, more predictable way. As Gallup explains:

And this isn’t new. Real estate usually claims the #1 title. But here’s what’s really interesting. This year’s results came in just after a rocky April for the stock and bond markets. It shows that, even as other investments had wild swings, real estate has held its ground. That’s likely because it gains value in a steadier, more predictable way. As Gallup explains:

“Amid volatility in the stock and bond markets in April, Americans’ preference for stocks as the best long-term investment has declined. Gold has gained in appeal, while real estate remains the top choice for the 12th consecutive year.”

That says a lot. Even though things may feel a bit uncertain in today’s economy, real estate can still be a powerful investment.

Yes, home values are rising at a more moderate pace right now. And sure, in some markets, prices may be flat in the year ahead or even dip a little – but that’s just the short-term view. Don’t let that cloud the bigger picture.

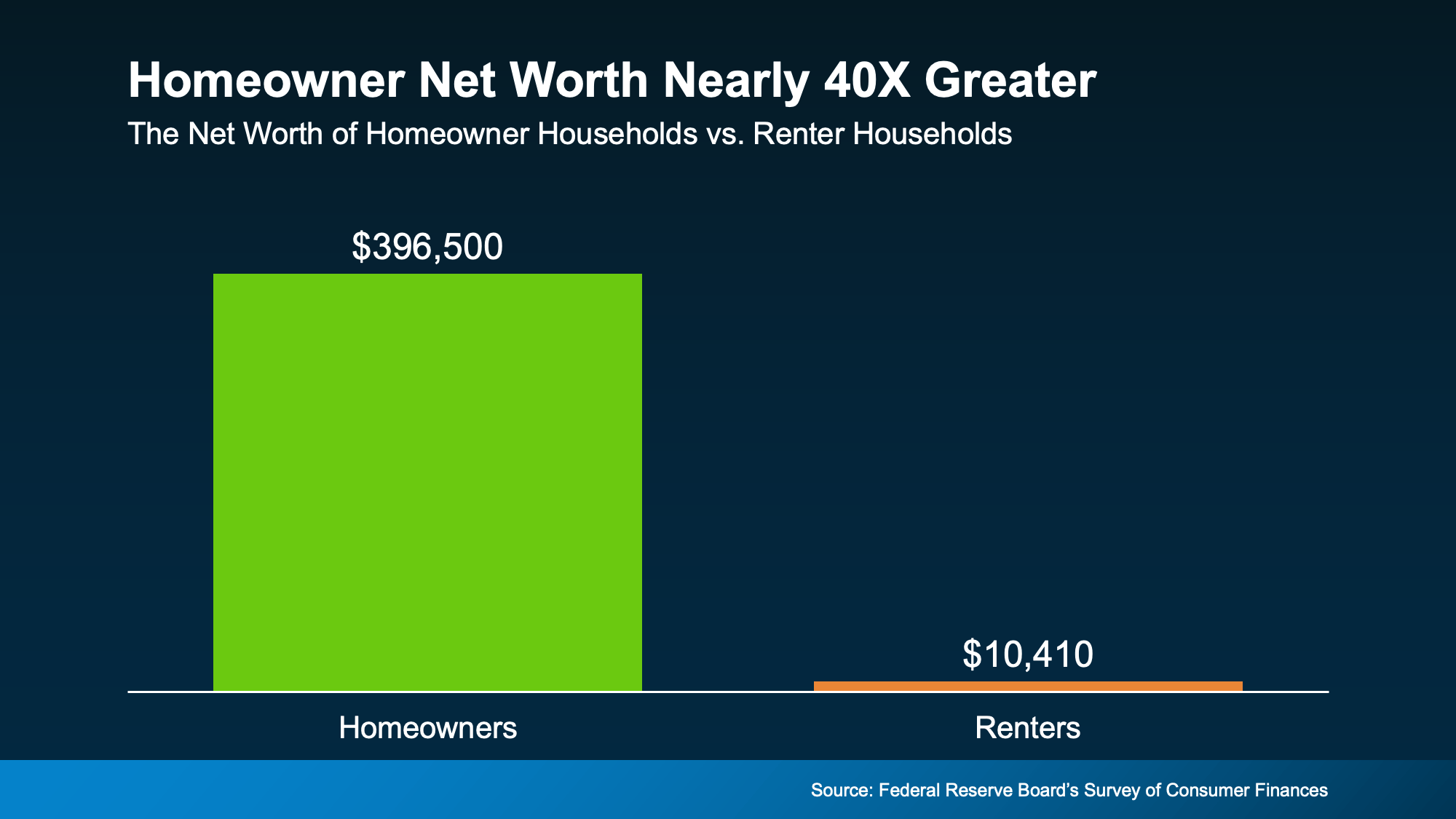

Real estate has a long track record of gaining value over time. That’s the kind of growth you can count on, especially if you plan to live in that home for a long time.

That’s part of why Americans continue to buy-in to homeownership – even when the headlines may sound a little uncertain. As Sam Williamson, Senior Economist at First American, says:

“A home is more than just a place to live—it’s often a family’s most valuable financial asset and a cornerstone to building long-term wealth.”

Bottom Line

Real estate isn’t about overnight wins. It’s about long-term gains. So, don’t let the uncertainty in a shifting market make you think it’s a bad time to buy.

If you’re feeling unsure, just remember: Americans have consistently said real estate is the best long-term investment you can make. And if you want more information about why so many people think homeownership is worth it, let’s chat.