Some homeowners hesitate to sell because they’ve got unanswered questions that hold them back. But a lot of times their concerns are based on misconceptions, not facts. And if they’d just talk to an agent about it, they’d see these doubts aren’t necessarily a hurdle at all.

If uncertainty is keeping you from making a move, it’s time to get the real answers. The ones you deserve. And to take the pressure off, you don’t have to ask the questions, because here’s the data that answers them.

1. Is It Even a Good Idea To Move Right Now?

If you own a home already, you may be tempted to wait because you don’t want to sell and take on a higher mortgage rate on your next house. But your move may be a lot more feasible than you think, and that’s because of how much your house has likely grown in value.

Think about it. Do you know anyone in your neighborhood who’s sold their house recently? If so, did you hear what it sold for? With how much home values have gone up in recent years, the number may surprise you. According to Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), the typical homeowner has gained $147,000 in housing wealth in the last five years alone.

That’s significant – and when you sell, that can give you what you need to fund your next move.

2. Will I Be Able To Find a Home I Like?

If this is on your mind, it’s probably because you remember just how hard it was to find a home over the past few years. But in today’s market, it isn’t as challenging.

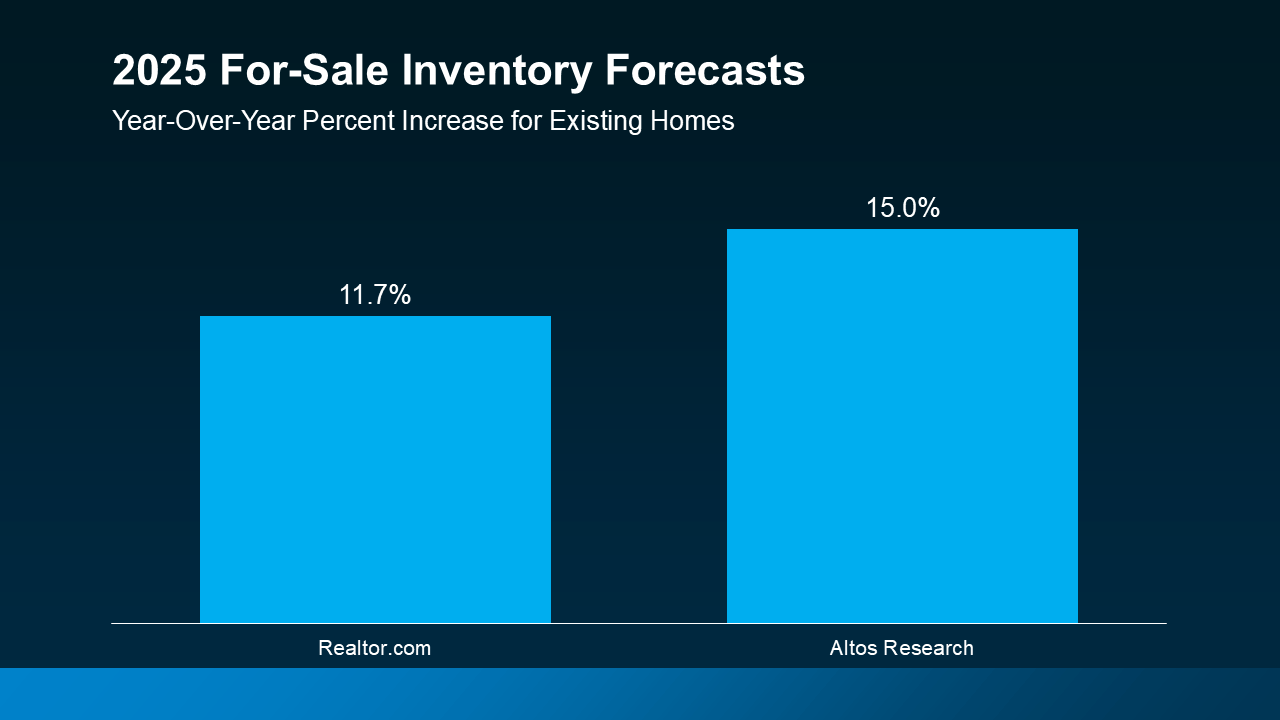

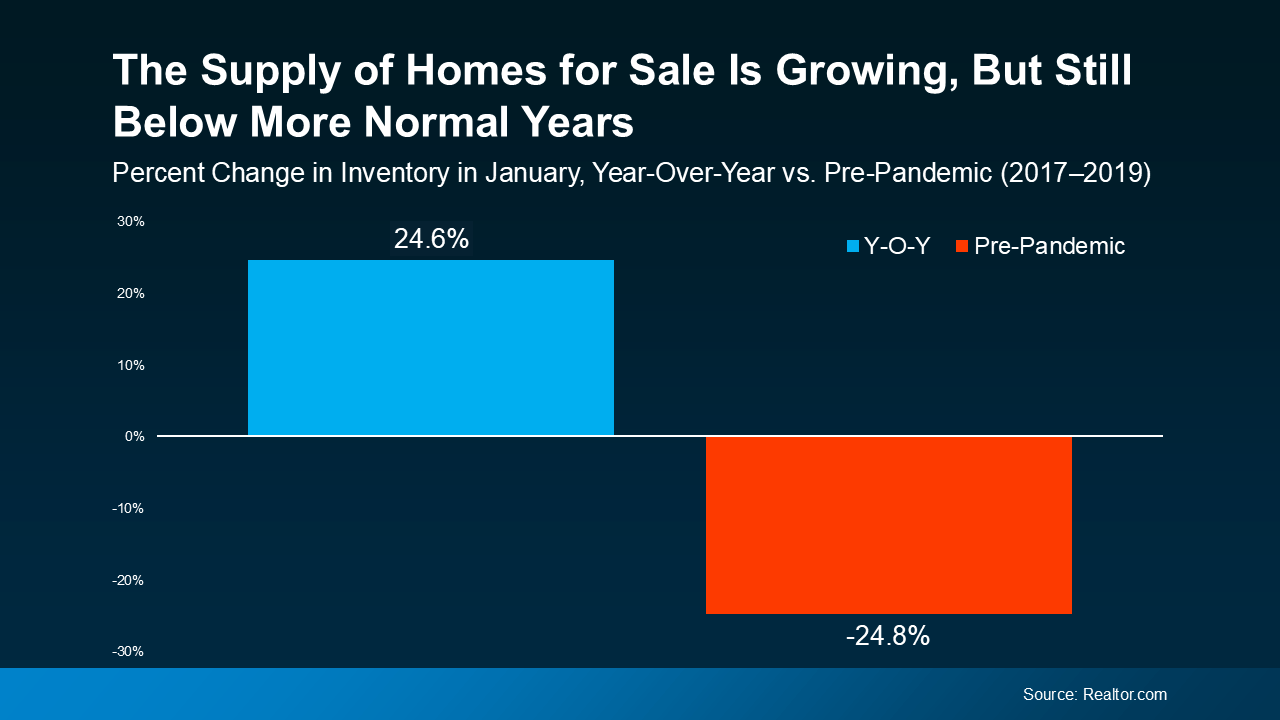

Data from Realtor.com shows how much inventory has increased – it’s up nearly 25% compared to this time last year (see graph below):

Even though inventory is still below more normal pre-pandemic levels, it’s improved a lot in the past year. And the best part is, experts say it’ll grow another 10 to 15% this year. That means you have more options for your move – and the best chance in years to find a home you love.

Even though inventory is still below more normal pre-pandemic levels, it’s improved a lot in the past year. And the best part is, experts say it’ll grow another 10 to 15% this year. That means you have more options for your move – and the best chance in years to find a home you love.

3. Are Buyers Still Buying?

And last, if you’re worried no one’s buying with rates and prices where they are right now, here’s some perspective that can help. While there weren’t as many home sales last year as there’d be in a normal market, roughly 4.24 million homes still sold (not including new construction), according to the National Association of Realtors (NAR). And the expectation is that number will rise in 2025. But even if we only match how many homes sold last year, here’s what that looks like.

- 4.24 million homes ÷ 365 days in a year = 11,616 homes sell each day

- 11,616 homes ÷ 24 hours in a day = 484 homes sell per hour

- 484 homes ÷ 60 minutes = 8 homes sell every minute

Think about that. Just in the time it took you to read this, 8 homes sold. Let this reassure you – the market isn’t at a standstill. Every day, thousands of people buy, and they’re looking for homes like yours.

Bottom Line

When you’re ready to walk through what’s on your mind, I have the answers you need. And in the meantime, tell me: what’s holding you back from making your move?