A lot of buyers are pressing pause on their plans these days, holding out hope that mortgage rates will come down – maybe even back to the historic-low 3% from a few years ago. But here’s the thing: those rates were never meant to last. They were a short-term response to a very specific moment in time. And as the market finds its footing again, it’s time to reset expectations.

Back in 2020 and 2021, 3% mortgage rates gave buyers a serious boost: more affordability, more buying power, and more opportunity. But those rates were a result of emergency economic policies during the height of a global pandemic. Now that the economy is in a different place, we’re seeing mortgage rates in the high 6% to low 7% range.

And while experts currently project a slight easing in the months ahead, most industry leaders agree: rates are not going back to 3%.

Instead, many forecasts suggest mortgage rates will settle in the mid-6% range by the end of the year, pending any major economic shifts. As Kara Ng, Senior Economist at Zillow, says:

“While Zillow expects mortgage rates to end the year near mid-6%, barring any unforeseen shocks, that path might be bumpy.”

What Buyers Should Know

Basically, waiting for 3% rates might mean waiting longer than you’d expect – and missing out along the way. Instead of putting off homebuying indefinitely, make a plan to get there and focus on what you can control: your budget, your credit, and working with a trusted professional who can explain exactly what’s happening in the current market – and how to navigate it.

Your local real estate agent and a trusted lender make all the difference in this process. The experts have insights into down payment assistance programs, alternative financing options, negotiation strategies, and overall – the experience you need on your side to understand creative ways that will make your plans work.

And here’s the biggest thing to keep in mind. Since rates are projected to ease slightly later this year, if that happens, it could bring some more buyers back into the market. Acting now gives you a head start, especially with more homes on the market than we’ve seen in years.

Think about it: if mortgage rates do come down, what do you think everyone else is going to do? That’s right – they’ll jump back in too.

Getting ahead of that rush could put you in a stronger position to find the right home with less competition. Realtor.com sums it up well:

“Staying out of the market in hopes of a rate drop that never comes can lead to missed opportunities . . . Rising home prices, rent increases, and inflation might outpace any future savings on interest. And if rates do fall sharply again, buyers could face an entirely different challenge: surging competition.”

Bottom Line

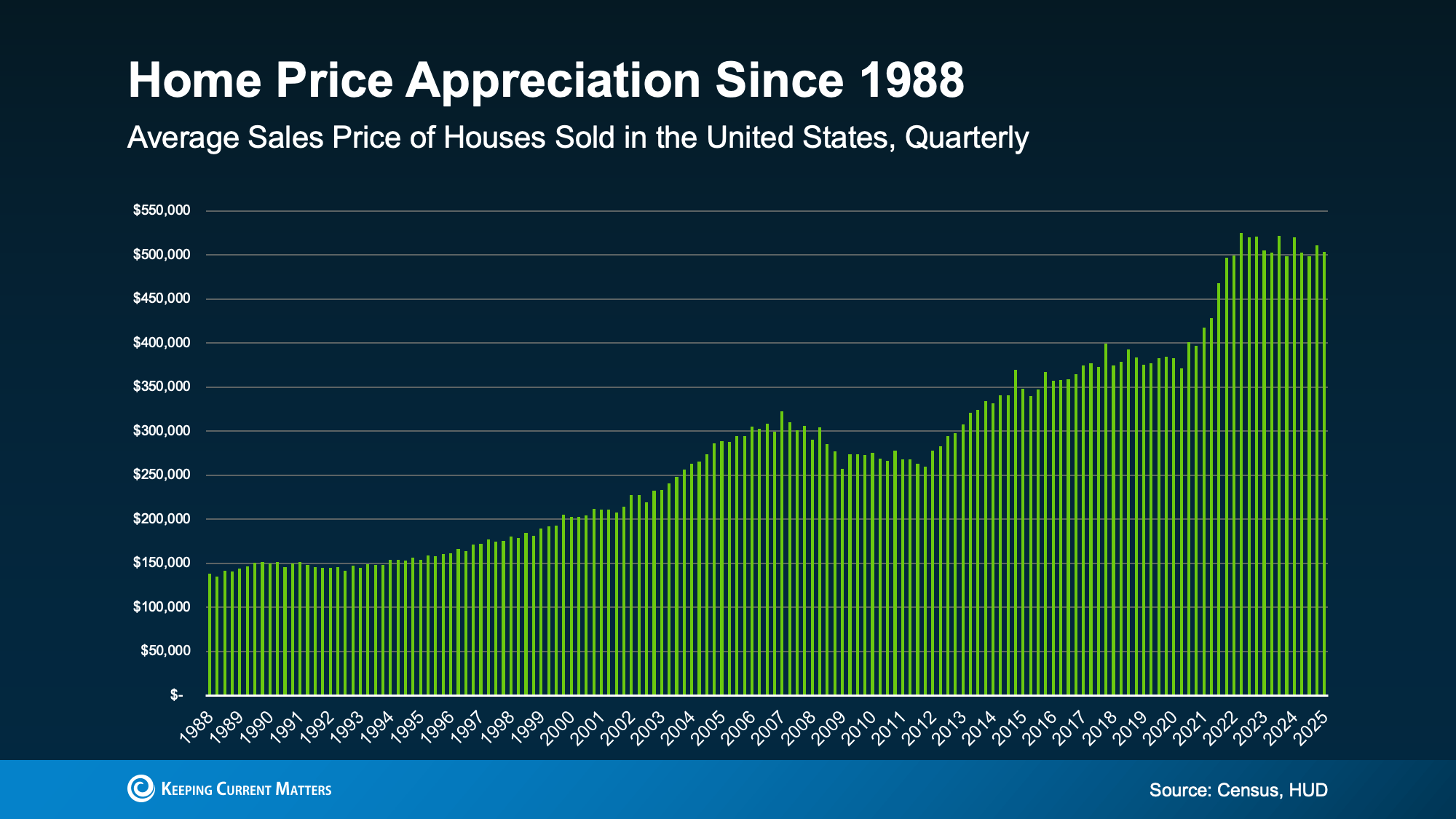

Those 3% rates everyone remembers from a few years ago were the exception, not the rule.

Now that they’re settling into new territory, it’s a good time to adjust your expectations and learn more about where things are heading as this market shifts.

A local real estate agent and a trusted lender will be your best resources, always keeping you up-to-date and informed, so you can make sense of your options and build a game plan that works for you.