If you’ve been frustrated by the lack of homes for sale over the past few years, here’s some good news. You have more options, so it may finally be time to kick off your home search again. As Daryl Fairweather, Chief Economist at Redfin, explains:

“Now is the best time to buy in the last two years. Mortgage rates are comparable to what they were two years ago, and prices remain high. However, there is significantly more inventory . . .”

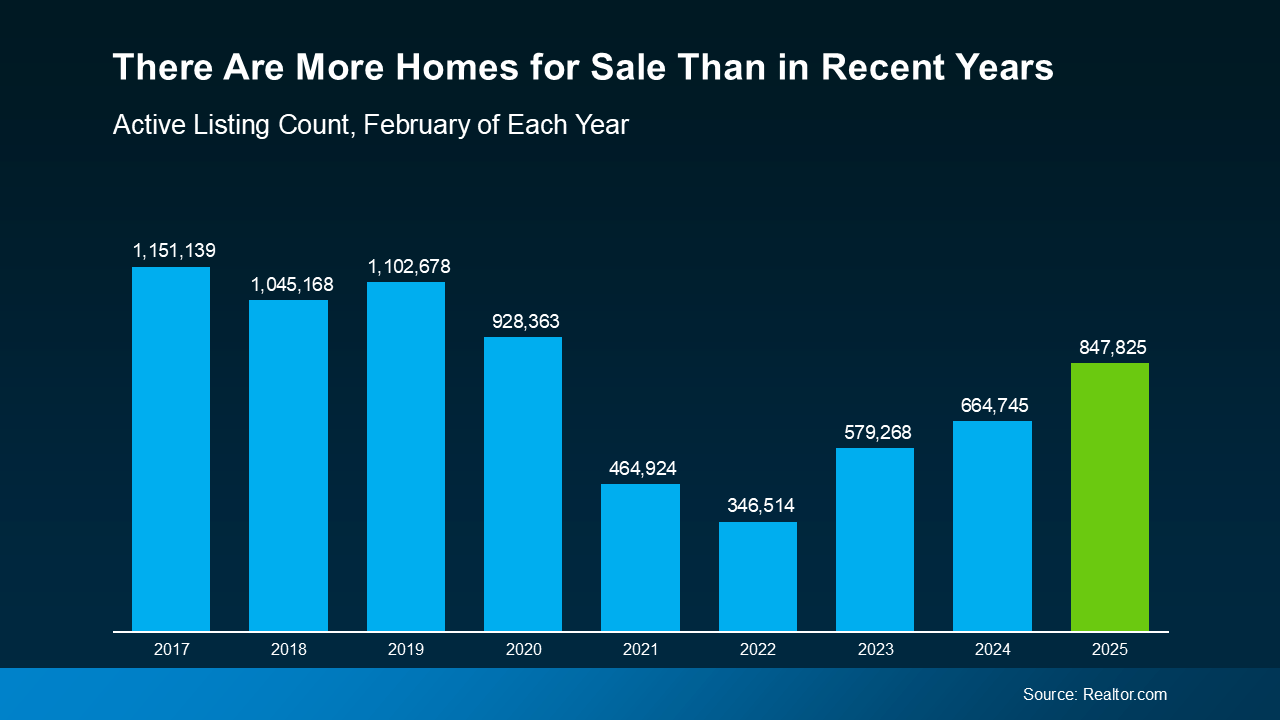

The number of homes for sale has grown compared to last year, and even more options are on the way. While this is typical for the busy spring season, here’s why this is so important right now.

Homeowners are listing their houses at the highest pace we’ve seen in a while.

New Listings Are on the Rise

Over the past few months, the number of new listings, or homes that have recently been put on the market for sale, has been steadily rising (see graph below):

Basically, more people are putting their homes on the market each month – whether they’re moving up, downsizing, or relocating. And this trend is a positive sign for the housing market.

Basically, more people are putting their homes on the market each month – whether they’re moving up, downsizing, or relocating. And this trend is a positive sign for the housing market.

Sellers who may have been on the fence the past few years are starting to jump back in. That’s helping to boost overall inventory and create better opportunities for both buyers and move-up sellers alike.

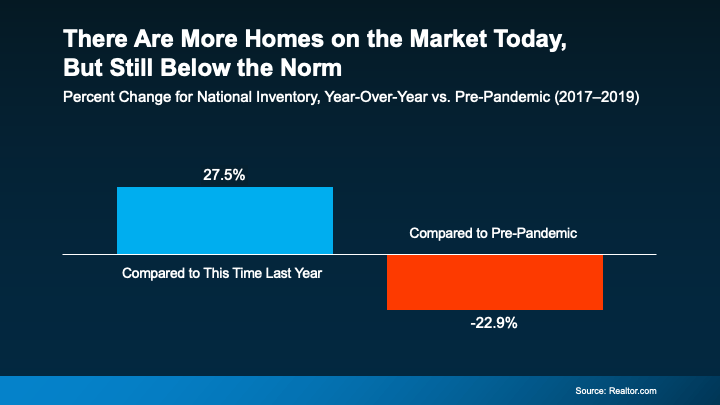

But it’s not just that the number of fresh options is up month-over-month; there’s also been a jump compared to last year.

According to Realtor.com, new listings in March were 10.2% higher than last year, making it the biggest March for new listings since 2021 (see graph below):

For anyone who’s been waiting for more choices, this is exactly what you’ve been hoping for – because more homes coming onto the market means more options and a better shot at finding one that fits your needs.

For anyone who’s been waiting for more choices, this is exactly what you’ve been hoping for – because more homes coming onto the market means more options and a better shot at finding one that fits your needs.

To make sure you don’t miss out on any of the latest listings for your area, lean on a local real estate agent.

Bottom Line

If you’re thinking about making a move this spring, now may be the time to start exploring your options. With more fresh listings hitting the market, you may find a home you love waiting for you.

What features or neighborhoods are at the top of your wish list?

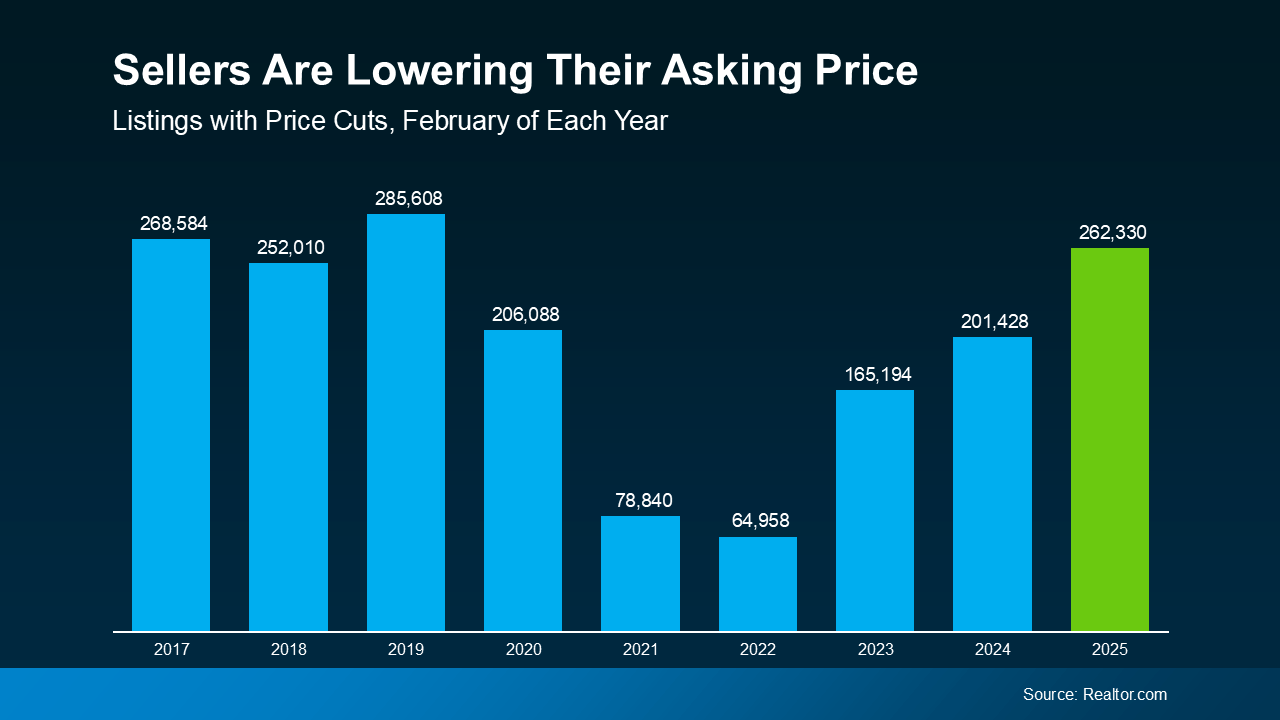

This is a sign sellers are more willing to compromise today. If you look back to more normal years in the market (2017–2019), you’ll see that the number of price cuts happening today is much closer to what’s typical – and for most buyers, that’s a big relief.

This is a sign sellers are more willing to compromise today. If you look back to more normal years in the market (2017–2019), you’ll see that the number of price cuts happening today is much closer to what’s typical – and for most buyers, that’s a big relief.